Does a Large One-Day Move in the S&P 500 Predict Next Week’s Return?

Large one-day moves make the S&P 500 feel more predictable than it is.

After a sharp rally, it is easy to feel late. After a sharp fall, it is easy to feel that something broke. In both cases, the temptation is to react immediately.

So I tested it.

The test is simple. Take every trading day in the S&P 500 Total Return Index from 1988 to 2026. Bucket each day by its one-day return. Then compound the next five trading days and take the median return in each bucket.

That gives one number per bucket: the typical next-week return after a given one-day move.

The setup

- Index: S&P 500 Total Return Index (

^SP500TR) - Period: 1988 to 2026

- Buckets: 1 percentage-point return buckets, with tail buckets at ≤ −5% and ≥ +5%

- Forward window: next 5 trading days

- Statistic: median next-week return

I use the median rather than the mean because the tail buckets are small and skewed. One extreme observation can move the mean too much.

Starting point

The analysis runs off one in-memory object. Building it is a separate job that depends on the data vendor. I pull from LSEG Workspace, which is licensed—the raw file and the cleaning logic stay off this page. The pipeline is the same one I described in an earlier post, with the universe set to the S&P 500.

daily—aSeriesof daily simple returns on the S&P 500 total-return series from 1988 to 2026, indexed by trading day. Total return, so dividends are reinvested back into the index level.

If you do not have an LSEG license, the equivalent open-data path is yfinance with ticker ^SP500TR (the S&P-published total-return index): pull Adj Close, take pct_change(), drop the leading NaN, and the rest of the post runs unchanged.

Parameters

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

HORIZON_DAYS = 5 # forward window in trading days (~one calendar week)Step 1. Buckets and the forward-return helper

BUCKETS = [

("≤ -5%", -np.inf, -0.050),

("-4%", -0.050, -0.040),

("-3%", -0.040, -0.030),

("-2%", -0.030, -0.020),

("-1%", -0.020, -0.010),

("+1%", 0.010, 0.020),

("+2%", 0.020, 0.030),

("+3%", 0.030, 0.040),

("+4%", 0.040, 0.050),

("≥ +5%", 0.050, np.inf),

]

def forward_cum_returns(s, lo, hi, k):

"""Compounded return over the k trading days AFTER each bucket event."""

# Left tail: exactly as labelled, r <= -5%

if np.isneginf(lo):

events = s[s <= hi]

# Right tail: exactly as labelled, r >= +5%

elif np.isposinf(hi):

events = s[s >= lo]

# Negative interior buckets:

# (-5%, -4%], (-4%, -3%], ..., (-2%, -1%]

elif hi <= 0:

events = s[(s > lo) & (s <= hi)]

# Positive interior buckets:

# [+1%, +2%), [+2%, +3%), ..., [+4%, +5%)

else:

events = s[(s >= lo) & (s < hi)]

out = []

for d in events.index:

idx = s.index.get_loc(d)

if idx + k >= len(s):

continue

forward = s.iloc[idx + 1: idx + k + 1].values

out.append(np.prod(1 + forward) - 1)

return np.array(out)Two design choices.

Boundary rules. The tail buckets are defined exactly as labelled: returns ≤ −5% go into the left tail, and returns ≥ +5% go into the right tail. The interior negative buckets are defined as (−5%, −4%], (−4%, −3%], …, (−2%, −1%]. The interior positive buckets are defined as [+1%, +2%), [+2%, +3%), …, [+4%, +5%). This assigns every included day to one bucket and avoids double-counting boundary days.

Skip incomplete windows. Events too close to the end of the sample are dropped, so every observation in a bucket has the same forward horizon. Filling forward NaNs with zero would silently bias the recent buckets toward zero.

Step 2. Aggregate per bucket

rows = []

for label, lo, hi in BUCKETS:

arr = forward_cum_returns(daily, lo, hi, HORIZON_DAYS)

rows.append({

"bucket": label,

"n": len(arr),

"median_pct": np.median(arr) * 100 if len(arr) else np.nan,

})

medians = (pd.DataFrame(rows)

.set_index("bucket")

.reindex([b[0] for b in BUCKETS]))Step 3. Chart

labels = medians.index.tolist()

y_vals = medians["median_pct"].tolist()

x_vals = list(range(len(labels)))

color = "#d62728"

fig, ax = plt.subplots(figsize=(14, 8))

ax.plot(x_vals, y_vals, "o-", color=color,

linewidth=2.5, markersize=9, zorder=5)

for xi, yi, lab in zip(x_vals, y_vals, labels):

offset_y = 14 if yi >= 0 else -16

ax.annotate(f"{yi:+.2f}%", xy=(xi, yi),

xytext=(0, offset_y), textcoords="offset points",

fontsize=10, ha="center",

va="bottom" if yi >= 0 else "top",

color=color, fontweight="bold")

ax.axhline(y=0, color="black", linewidth=1.0, zorder=1)

ax.set_xticks(x_vals); ax.set_xticklabels(labels, fontsize=12)

ax.set_xlabel("Single Day Return", fontsize=14)

ax.set_ylabel("One Week Return (%)", fontsize=14)

ax.set_title("One Week After a Single Day Return",

fontsize=18, fontweight="bold")

ax.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()Results

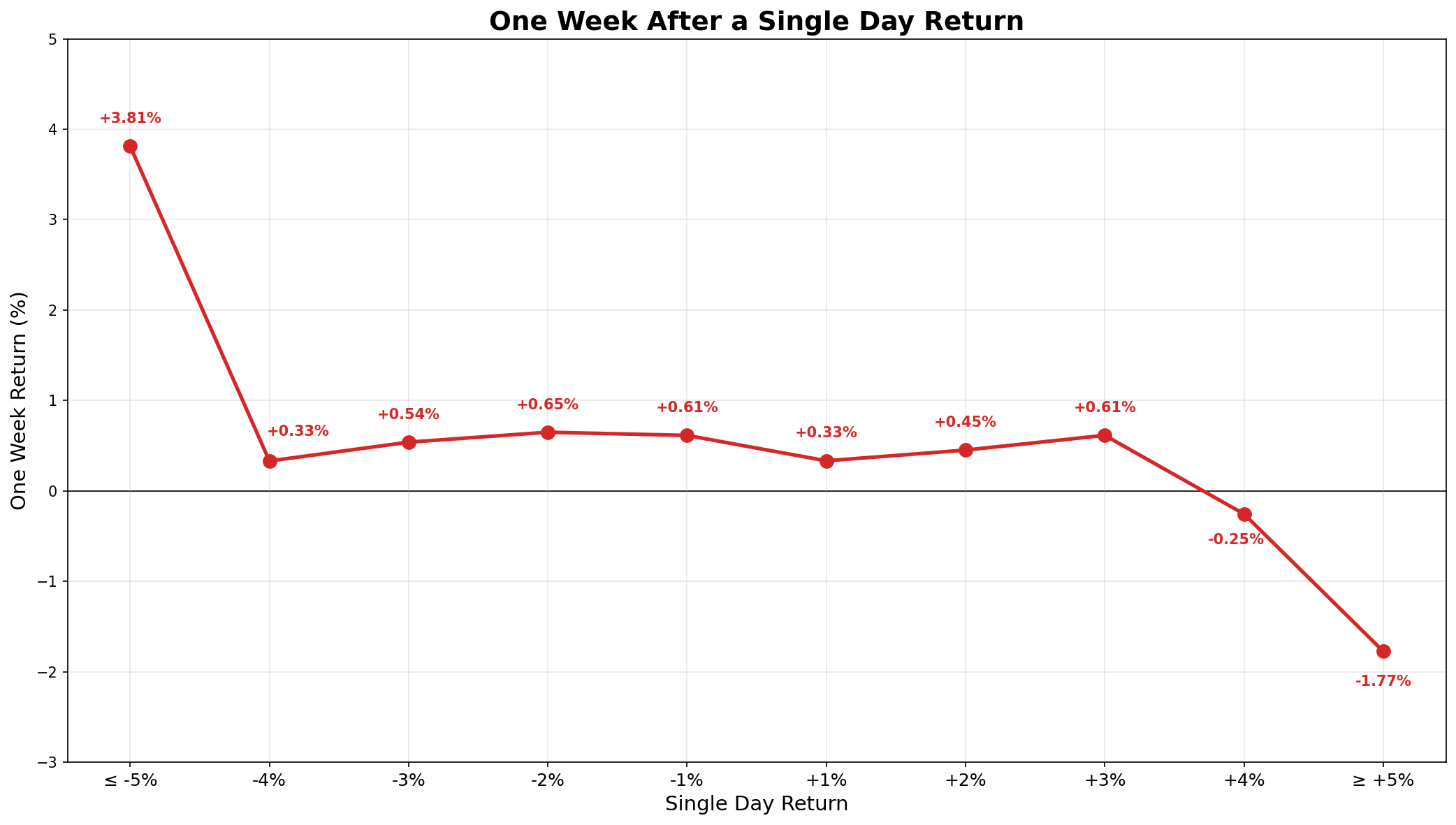

After a ≤ −5% day, the median next-week return is +3.81%.

After a ≥ +5% day, it is −1.77%.

The middle buckets are much less interesting. Most sit close to zero and close to the unconditional 5-day forward median of +0.39%.

The signal is at the tails. The middle buckets show little obvious signal.

This does not mean every large down day should be bought or every large up day should be sold. It means that, historically, the median next-week return moved against the initial one-day move at the extremes.

The reversal after large down days is larger than the reversal after large up days. That asymmetry should not be overstated. The extreme buckets are small and dominated by crisis periods.

Caveats

Thin tails. The extreme buckets are small. Over 1988 to 2026, the ≤ −5% bucket contains 23 events and the ≥ +5% bucket contains 21. These observations cluster around crisis periods such as 1987, 2008, and March 2020. The tail estimates should therefore be read as suggestive, not stable laws.

Overlapping windows. Large moves often arrive in clusters. If two extreme days occur close together, their next-5-day windows overlap. That means the observations are not fully independent.

No execution assumption. This is not a tradable strategy. It does not specify whether the trade happens at the close, the next open, or some other price. It also ignores spreads, slippage, and implementation.

Median, not strategy return. The chart shows the median next-week return conditional on the previous day’s move. It does not show the return from a portfolio rule. A rule that only trades after ±5% days would trade very rarely.

One index, one sample. The result is for the S&P 500 Total Return Index from 1988 to 2026. Other markets, other horizons, or other samples may look different.

Data source

S&P 500 Total Return Index, pulled from LSEG Workspace (licensed). Dividend reinvestment is built into the index level itself, so the daily simple return from pct_change() reflects a reinvesting investor. The download pipeline is in an earlier post. Free equivalent: Yahoo’s ^SP500TR via yfinance.

Disclaimer: hypothetical analysis on a historical total-return series, for discussion purposes only. Not investment advice. Past performance does not predict future returns.